INNO Accounting services

Vietnam prepaid expenses

Main content

What are prepaid expenses?

Prepaid expenses are purchased and paid once but used for many periods.

What goods and services are recorded as prepaid expenses?

Goods and services are recognized as prepaid expenses when:

– Goods and services purchased and used for many periods.

– Goods and services are not eligible for recognition of fixed assets.

Read more: Conditions for recognition of fixed assets

Why we need to allocate prepaid expenses?

Prepaid expenses are not counted at one time but allocated into many periods because such expenses are purchased and used in many periods, so to ensure the appropriate principle of accounting, expenses should be allocated according to the corresponding number of usage periods.

Prepaid expense allocation time

Depending on the usage period of the prepaid expenses that the enterprise allocates in an appropriate period. However, the maximum prepaid expense allocation period is 36 months (3 years).

Accounting bookkeeping for prepaid expenses

When purchase a prepaid expense

Debit 242 – Prepaid expense: the amount spent (excluding VAT)

Debit 1331 – Creditable VAT: VAT amount on invoice

Credit 111, 112, 331 : total payment

Periodically allocation

Debit 621, 622, 627, 641, 642… – Expense accounts depend on the purpose use: allocated amount per period

Credit 242 – Prepaid expense

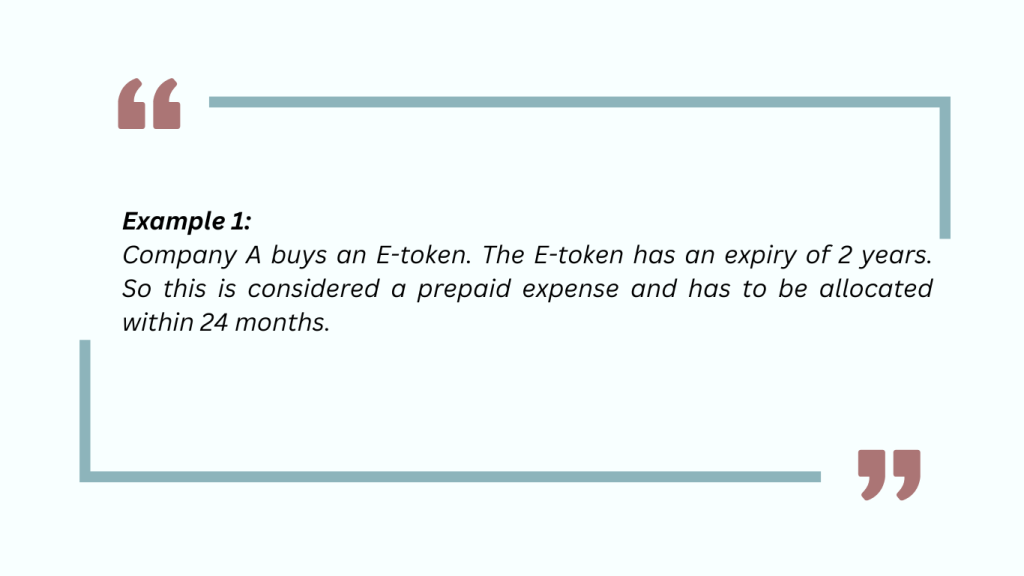

Example:

Company A purchases an e-token for VND 2,000,000 (excluding 10% VAT). The e-token has an expiration of 2 years. The company paid in cash. So this is considered a prepaid expense and has to be allocated within 24 months.

When purchase the E-token:

Debit 242: 2,000,000

Debit 1331: 200,000

Credit 1111: 2,200,000

Periodically allocation:

Debit 642: 83,333

Credit 242: 83,333

Share the post

Explore more

Related services

News

Related Posts